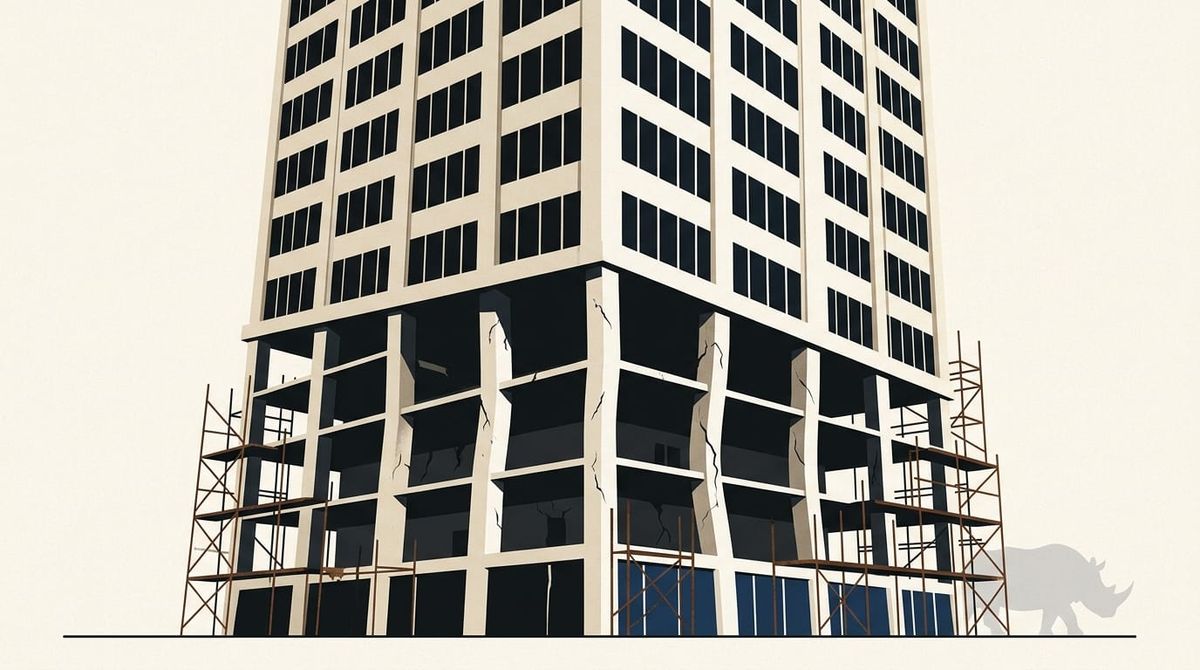

A trillion dollars in commercial property loans comes due in 2026–27, refinancing from 3–4% into 6–8%. Community and regional banks hold 70% of it — and one failure could force them all to mark down similar loans together.

About $1.2 trillion in commercial property loans come due in 2026 and 2027. Most were made at 3–4% and must now refinance at 6–8% — roughly doubling the monthly cost at a time when office values have fallen about 38% from their peak. Community and regional banks hold about 70% of these loans, and many sit above the Fed's informal warning line of property loans worth more than 300% of their safety cushion.

The market underprices this because regional bank shares trade cheap but haven't priced a real credit event. Our estimate puts yearly losses near $47 billion, about 3.9% of the trillion at stake. One failure can force every bank to mark down similar loans at once.

New York Community Bancorp already took heavy office and apartment losses. Valley National Bancorp, Columbia Banking System, Western Alliance Bancorporation, and Zions Bancorporation all carry heavy property concentrations relative to their capital, leaving each exposed if borrowers can't refinance at the new, higher rates.

Why this matters. About $1.2 trillion in commercial property loans come due in 2026–27 and must refinance at roughly double their old rate, which many buildings can't afford from rent. Community and regional banks hold 70% of these loans, so the pain lands on smaller lenders — and their depositors and shareholders — not the giant banks. Any lender, building owner, or investor near this exposure should care because one failure can force every bank to mark down similar loans at once.

Blindside · US Macro Risk

Bank Loans Reset at Triple the Rate

A trillion in property loans comes due at double the cost

Imminent

74

Blindside index

What drives it — drag to test

each slider starts at our cited estimate — drag to see the range

Share of maturing loans that go bad8%

Sourced — MSCI's property distress rate hit 8.3% early 2024; regulators flag rising office risk.

How many cents are lost on each bad loan40%

Sourced — Moody's puts office losses at 35–50%, apartments at 20–30%; blend near 40%.

Damage spreading to loans not yet due+15%

Our judgment — regulators forcing wider loan reviews could push losses past the loans coming due.

Time to impact

1–3 yearsImminent

now3 yrs7+ yrs

When the financial hit begins to land, on our read.

How to read this. Drag any slider to test your own number — the chart and index update live. The likelihood and the locked facts stay put.

Yearly loan losses, most likely case

$47.2bn3.93% of sector

Dark line = most likely · faint lines = low–high (8 in 10 outcomes land between) · shaded band = what outside analysts expect

Our estimate lands within what outside analysts expect ✓

Chance this is a permanent shift, not a blip

66%

Average of five independent reads (range 52–78%):

The track record72%

Past property downturns saw 8–12% of loans go bad; 2009 hit 11% with smaller rate jumps.

How it works78%

The math is fixed: repricing $1.2 trillion from 3% to 7% adds about $48 billion in yearly costs rents can't cover.

The skeptic's case52%

Banks have stalled before; rate cuts could narrow the gap; apartment loans stay easy to sell.

What regulators say68%

The two main bank watchdogs both warned about property concentrations in 2023–24, signaling they see it coming.

What the market shows60%

Regional bank shares trade cheap but haven't priced a real credit hit; loan-bond spreads widened but stay below 2009.

Fixed — the sliders change the size of the hit, not the odds it's permanent.

Why this matters

About $1.2 trillion in commercial property loans come due in 2026–27 and must refinance at roughly double their old rate, which many buildings can't afford from rent. Community and regional banks hold 70% of these loans, so the pain lands on smaller lenders — and their depositors and shareholders — not the giant banks. Any lender, building owner, or investor near this exposure should care because one failure can force every bank to mark down similar loans at once.

Most exposed companies

New York Community Bancorp NYCB · Valley National Bancorp VLY · Columbia Banking System COLB · Western Alliance Bancorporation WAL · Zions Bancorporation ZION

🔒

The facts — locked

measured, not editable

$1.2T

Roughly $1.2 trillion in commercial property loans come due between 2026 and 2027.

Mortgage Bankers Association / Trepp CRE Maturity Monitor (2024)

300%+

Many regional and community banks hold property loans worth more than 300% of their safety cushion — the Fed's informal line for closer watch.

FDIC Quarterly Banking Profile, Q4 2024

8.3%

MSCI's commercial property distress rate hit 8.3% in early 2024, the worst since 2013.

MSCI Real Assets / RCA (Q1 2024)

3–4% → 6–8%

Loans made in 2019–22 at 3–4% must now refinance at 6–8%, roughly doubling the monthly cost.

Trepp CRE Research (2024)

70%

Community and regional banks hold about 70% of all outstanding property loans, piling the risk outside the biggest banks.

Federal Reserve Board CRE Concentration Report (2023)

$38bn

Office building values fell about 38% from their peak by early 2024 — the part of the market most exposed to the 2026–27 wave.

Green Street Advisors Office Value Index (March 2024)

Attention is climbing. the market is starting to price this in — the early window is closing.

Roughly $1.2 trillion in commercial property loans mature in 2026–27, most made at 3–4% and now refinancing at 6–8%, doubling the monthly bill. Our bottom-up estimate puts realized losses near $47 billion a year, within a $35–62 billion range — about 3.9% of the $1.2 trillion at stake. The blind spot: regional banks holding 70% of this exposure, many above the 300%-of-capital line, have priced in a soft landing, and one large community-bank failure could force every bank to mark down similar loans together.