The Market Paid for the Steel, Not the Story: H1 2026’s Brutal Tech Split

Across 21 hype themes tracked in H1 2026, silicon and substations surged while software, crypto, and memes sank. Wall Street stopped paying for pure narrative and shifted capital directly to physical infrastructure, hardware, and firms that actually ship physical products.

The Tape

The 21 themes FASTMaster is tracking are hype baskets — the stories Wall Street trades, not the tidy sectors a textbook files them under. In the first half of 2026, the punchline was that stories stopped paying: the market handed its richest rewards to the names that fabricate the AI buildout and took the back of its hand to the ones merely running software on top. The chip basket finished up 73.8% while the crypto basket sat dead last — proof the market stopped paying for the story and started paying for the steel.

The Board

- AI — the silicon (+73.8%): Top of all 21 — Arm Holdings, the firm whose chip designs sit inside nearly every phone on earth, more than tripled at +231.9% over six months, the single loudest verdict on our board.

- AI Power (+69.9%): When a theme's slowest name is still up, the theme worked — data-center plumbing took second, led by Powell Industries, maker of the electrical switchgear that feeds server halls, at +150.8%.

- Space (+52.2%): Frontier tech that bills for service today — Iridium, the satellite-network operator, rocketed +166.4% on an Oppenheimer upgrade, carrying the basket to third of 21.

- AI + Tech (+26.8%): A blended megacap-and-AI basket that rose on its chip exposure even as Salesforce, the cloud-software giant, shed 34.6% touting an AI it couldn't sell to the tape.

- Psychedelics (+24.0%): A thin six-name theme that split hard on data — Compass Pathways climbed 84.4% after a narrowed quarterly loss beat estimates, because the clinic, not the press release, gets paid here.

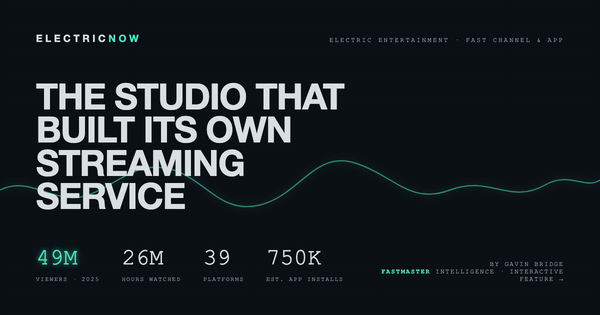

- Entertainment (+11.4%): The steadiest theme on the board, with the smallest drawdown of the 21 — Sphere Entertainment rose 62.5% as 'The Vampire Lestat' took over its Las Vegas venue, spectacle that actually fills seats.

- Biotech (+4.8%): Barely green and quietly divided — Moderna gained 61.7% on pipeline progress, including a Lynch-syndrome cancer trial, the vaccine maker reborn as a pipeline story.

- Robotics (+1.5%): Flat on top, brutal below — Teradyne, which builds the gear that tests semiconductors, nearly doubled at +94.3%, as robotics money again flowed to the company selling picks to the chip boom.

- Sports & Betting (−0.2%): Dead flat as a theme but wide underneath — Rush Street Interactive rose 53.3% eyeing new markets in Canada and Rhode Island, a reminder that not all betting is the same bet.

- Music (−0.5%): Roughly flat, with the owners beating the operators — Reservoir Media, a music-rights holder, climbed 37.0% on an earnings beat, because owning the catalog still pays better than streaming it.

- Defense + Drones (−1.4%): Flat as a theme, split by results — Leonardo DRS, the defense contractor, gained 39.5% on a 25.9% earnings beat, the prime that delivered numbers and not just order announcements.

- Weight-Loss (−3.3%): The obesity-drug trade cooled as the field crowded — Terns Pharmaceuticals, an early-stage entrant, jumped 71.4% while later arrivals queued for a shrinking lane.

- Gaming (−4.0%): A losing theme with wild extremes — Skillz, the mobile-gaming contest platform, nearly doubled at +95.7%, a small turnaround bid in a basket its biggest names dragged down.

- Hype Goods (−5.7%): Consumer hype split by price tag — Crocs gained 43.4% on sold-out collabs like LoveShackFancy, the cheap, viral product that kept ringing the register while pricier names didn't.

- Fast Food (−8.5%): A down theme where the expansion story still ran — Cava Group, the growing Mediterranean chain, rose 50.3% while maturing peers had their multiples quietly repriced.

- Emerging Therapeutics (−9.7%): A bruised early-stage basket with one name left standing — Intellia Therapeutics, the gene-editing developer, held a 31.5% gain while the rest priced for patience, not promise.

- Nuclear Energy (−11.1%): The power theme split on the order book — GE Vernova rose 38.4% on $18 billion of orders in a single quarter, backlog the market believed where a softer fuel name's outlook it didn't.

- Quantum (−14.8%): The frontier the tape still won't fund, and the deepest drawdown of the 21 — IonQ rose 23.7% on a $39M space-agency deal but rode 108% volatility to get there.

- Tech — software / SaaS (−16.9%): The application layer the market shorted while it bought the chips — Intuit, owner of TurboTax and QuickBooks, lost 56.0% amid an investor probe, the SaaS bellwether the AI era repriced hardest.

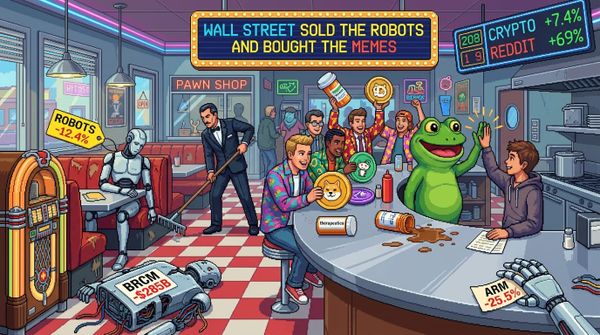

- Meme Stocks (−24.0%): Second-worst of the 21, where pure narrative got the short shrift — Lucid Motors fell 53.4%, rolling out hands-free driving while the stock did nothing but reverse.

- Crypto (−36.2%): Dead last of all 21 — even Dogecoin, the basket's least-bad name, fell 24.3%, and when the leader is down a quarter, the market follows.

The Stories

The Chip Tripled and the Software Sank

The tidy version — "AI is up" — misses the half's real lesson. The market did not buy AI. It bought the half of AI you can drop on your foot.

The silicon basket finished first of our 21, up 73.8%. Arm Holdings, whose chip designs sit in nearly every phone, more than tripled. Marvell and Micron, the networking and memory names, each rose more than 200% in H1.

Now the other half. The software/SaaS basket finished 19th of 21, down 16.9%. Intuit, the TurboTax owner, lost 56.0%. Adobe shed 38.8%, Salesforce 34.6%.

The split even ran inside the silicon basket itself. Its leaders fabricate things; its one laggard sells software — and was the only name in the group that fell. Palantir, the data-analytics firm, dropped 23.8%, C3.ai 20.7%.

In fairness, the application layer is where AI is supposed to earn its keep eventually. The market simply declined to pay today for a return promised tomorrow.

Salesforce spent the half touting its Agentforce AI; the stock spent the half falling. Alphabetwas the lone software name to rise, up 14.1% — and notably, it's the one backing the chips, with a $35 billion arrangement behind Anthropic. Even the software winner won by association with the steel.

Space Ships Payloads, Quantum Ships Slides

Two frontier themes, two opposite verdicts, one rule connecting them: the market now grades the future on whether it can invoice the present.

Space finished third of 21, up 52.2%. Iridium, which runs a satellite network and bills customers for service today, jumped 166.4% on an Oppenheimer upgrade. Redwire rose 67.4% and BlackSky 55.7% — names that put hardware in orbit for revenue.

Quantum finished 18th, down 14.8%, with the deepest drawdown on the board, nearly half from peak to trough. Arqit Quantum, an encryption hopeful, fell 44.6%. SEALSQ lost 26.9%, Quantum-Si 18.4%.

The difference isn't the physics. It's the invoice. Space sells payloads; quantum still mostly sells partnerships and conference slides.

Not that quantum was uniformly punished. IonQ rose 23.7% on a $39M space-agency deal and DARPA work — but it rode 108% volatility to get there, which is the market's way of saying it isn't sure either.

The future may well be quantum. The first half of 2026 simply asked it to ship something first.

The Plumbing Beat the Poker Table

If H1 2026 had a thesis, it was this: physical infrastructure beat speculation, and the gap was a canyon.

The data-center buildout's unglamorous supply chain — the AI Power basket — finished second of 21, up 69.9%. Powell Industries, which builds the electrical switchgear that feeds server halls, gained 150.8%. Astera Labs rose 104.5%, Coherent 98.1%. Even the slowest name, the data-center landlord Digital Realty, rose 18.8%.

At the other end of the board sat the pure-narrative trades. Crypto finished dead last of 21, down 36.2%. Avalanche and Cardano each fell 45.0%, Solana 42.9%. Meme Stocks landed second-to-last, down 24.0%.

Notice what the winners had in common: they all make a physical thing someone needs to build a data center. Notice what the losers had in common: a story and a ticker.

There were exceptions, and they prove the rule. The one meme name to rise, Novavax, climbed 24.5% — because it had an actual product, a Sanofi flu-COVID shot, behind it. Avalanche even floated a treasury-strategy vehicle onto Nasdaq; the token fell anyway. Listing the company is not the same as earning.

The market spent the half-year voting. It voted for steel.